Latin American Aftermarket Trends & Insights Categories: 2025, 2025, News Timelines: Argentina, Brazil, Central America, Chile, China, Colombia, France, Germany, India, Italy, Mexico, Morocco, Peru, Poland, Portugal, Russia, South Africa, Spain, Thailand, Turkey, United Kingdom, Vietnam

Announcement Date : 17 March 2025

Latin American Aftermarket Trends & Insights

The Latin American aftermarket is shaped by several macroeconomic factors, regulatory environments, and regional trends. The total car parc across the three largest markets—Brazil, Mexico, and Argentina—accounts for 89 million vehicles. The sector is expected to grow at an average rate of 8% by 2025, with significant variations in each country.

-

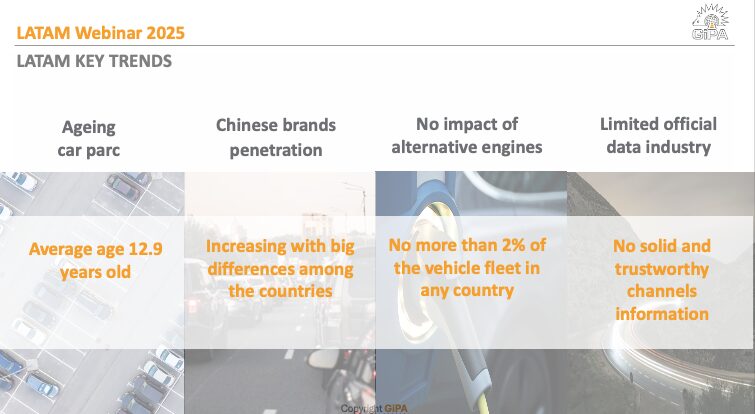

- Vehicle Car parc Aging & Growth

According to GiPA’s forecast:

- By 2027, 59% of the region’s car parc will be over ten years old.

- The current average vehicle age is 12.9 years, increasing the demand for aftermarket services and replacement parts.

- Light commercial vehicles (LCVs) form an essential part of the car parc in Argentina and Mexico, especially with the rising popularity of pickups.

This aging trend creates a strong demand for traditional maintenance and repair services, driving business opportunities in parts manufacturing and distribution.

- Penetration of Chinese Vehicle Brands

Chinese brands are reshaping the competitive landscape across different Latin American countries:

- Chile has the highest penetration, with 30% of new registrations coming from Chinese brands due to lower import tariffs and competitive pricing.

- Mexico has seen a surge in Chinese automakers, influencing consumer purchase behavior and long-term service needs.

- Argentina has had minimal Chinese brand penetration due to past economic conditions, but with the changing policies, it is expected to evolve.

While electric vehicles (EVs) are often associated with Chinese brands, their penetration is still primarily in the gasoline vehicle segment.

- Alternative Powertrain Adoption & Infrastructure Challenges

The region’s transition to alternative energy vehicles remains slow. The key insights on EVs include:

- EV adoption is at 7% in the U.S. but remains at only 2% in Latin America.

- The lack of charging infrastructure is a major bottleneck, particularly in Mexico, where the electrical grid is not prepared for mass EV deployment.

- Government policies still favor traditional energy sources, limiting EV market growth.

Despite media reports of double-digit EV growth, penetration remains marginal due to high costs, infrastructure gaps, and consumer preferences.

- Digitalization & Online Sales Growth

Digital transformation is reshaping the aftermarket in Latin America. Insights from the discussion highlighted:

- 58% of U.S. consumers buy auto parts online, while Latin America is still catching up.

- Mexico, Brazil, and Argentina show high digital engagement for research but lower digital purchase conversion rates.

- E-commerce platforms like Mercado Libre dominate online auto parts sales, but industry-specific platforms are still underdeveloped.

- Workshop networks and B2B e-commerce adoption remain fragmented, highlighting a need for standardized digital procurement systems.

- Market Structure & Competitive Landscape

The Latin American aftermarket presents a diverse market structure, with key differences across countries:

- Brazil: Highly fragmented with regional logistics challenges, requiring strong distributor networks.

- Mexico: A growing independent aftermarket (IAM) sector, supported by high vehicle longevity and traditional combustion engines.

- Argentina: Facing policy-driven fluctuations, yet showing resilience in maintenance demand due to an aging car parc.

IN DETAILS:

ARGENTINA

Argentina is a country of constant change—perhaps a perfect example of what it means to face ongoing challenges and continuous movement. We are in a period of transition, a time of macroeconomic and political change, shifting direction, redefining our course. Argentina has moved from being a very closed country, with restricted borders, limited availability of goods, and few imports, to a completely open model that prioritizes competition, has opened its borders, and is now deregulating and liberalizing almost everything. We are in the middle of this transformation.

What is the outlook? What is the direction for the coming years? It is challenging to predict, and it is difficult to define clear metrics.

One fundamental factor is the size of the vehicle car parc—the number of cars in circulation in Argentina that require parts and maintenance. This is an objective fact, independent of political or economic contexts.

Currently, there are 11 million vehicles in Argentina. If we look back ten years, that number was less than 8 million. This indicates a growing market with expanding opportunities. These 11 million vehicles define the aftermarket landscape, with a particular characteristic: 2.5 million of them are light commercial vehicles.

This is mainly driven by the popularity of locally manufactured pickup trucks, which have seen significant growth in recent years. Pickups are no longer just used for work or commercial purposes but have also been adopted by households. Due to the limited availability of other vehicle options and the benefits of purchasing Argentina-made pickups, many families have incorporated these vehicles into their daily lives.

These vehicles have high mileage, heavily worn engines, and drivers with fewer financial resources who are also more digitally engaged, adopting a more DIY (do-it-yourself) approach. There are many aspects to consider in this rapidly evolving market.

Another crucial factor is usage levels, which define product replacement intervals and determine how often users visit workshops. Having this data is essential. In Argentina, the average annual mileage is 10,535 kilometers. This number, which is fundamental in shaping the aftermarket’s needs, was around 14,000 kilometers ten years ago. It has been declining, just as it has globally, due to discouragement, alternative transportation options, but especially in Argentina due to the economic crisis and rising fuel costs.

Despite this, in terms of workshop visits, users visit nearly every three months—quite frequently. If we look only at passenger cars, there are 22 million workshop visits per year. If we include light commercial vehicles, that number rises to nearly 30 million visits. So, even with declining usage levels, the market remains highly attractive.

We talked about car parc aging, but another key trend is the increasing retention of vehicles. Drivers are keeping their cars for longer periods. This presents an opportunity for businesses to focus on customer loyalty, as there is now more time to capitalize on retention strategies. Previously, the average car owner kept their vehicle for four years, but this has now extended to five years, and for light commercial vehicles, it’s close to six years. This opens up more opportunities for customer loyalty efforts, emphasizing factors such as durability and long-term maintenance.

There are a few key factors to keep in mind when considering business opportunities in Argentina:

- Financing is essential.In some markets, this is taken for granted, but in Argentina, financing creates opportunities. During inflationary periods, the ability to pay in installments allowed consumers to access desired products. Even in today’s more stable environment, financing remains critical—it enables consumers to plan their purchases, such as a new battery, which they might not be able to afford outright but could manage in three or six installments.

- In times of crisis, promotions and timing are key.Marketing strategies and communications should emphasize promotional opportunities to attract consumers.

- Adapting to an aging vehicle car parc is crucial.Product portfolios, business strategies, and messaging must align with the reality of an older car market.

- Digitalization is a vital tool.Economic uncertainty, inflation, and constant change mean that Argentine consumers are always looking for guidance, often turning to digital tools for information. Even if they don’t finalize a purchase online, they research pricing, brands, product specifications, and service providers. A strong online presence is necessary to maintain market relevance.

- Accident rates present a business opportunity.Unfortunately, Argentina has a high accident rate—18%—which translates into strong demand for bodywork repairs, a segment with a high average ticket price.

Now, if you’ll allow me, let’s cross the Andes and move on to Argentina’s neighbor, Chile. And beyond the mountains, at times, it feels like an abyss separates the two countries. All the volatility and dynamism we’ve discussed about Argentina contrast with a highly structured, forward-looking, and stable Chilean market.

While Argentina is just beginning to open up after years of protectionism, Chile is the kingdom of competition and free trade. It is an extremely open market, currently hosting 70 different car brands from all over the world. It serves as a testing ground for global brands, with 30 of these 70 brands being Chinese. Nearly 30% (29.6%) of new vehicle registrations in Chile are Chinese-made. Tesla also chose Chile as its first entry point into South America.

However, despite the large number of brands, Chile’s market is highly concentrated when it comes to distribution.There are a few dominant import groups that handle multiple brands, creating a different market structure than Argentina. Unlike Argentina, where local manufacturing and protectionist policies dominate, Chile’s market is controlled by large import companies that manage several brands at once.

This structure has also led to the development of service networks. These include dealer networks, repair shop networks, and spare parts networks, which help professionalize the aftermarket industry. This addresses a key gap in South America: the need for professionalization, better access to technical information, training, and equipment. Chile is one of the most advanced countries in Latin America when it comes to structured service networks.

Despite having a car parc of under six million vehicles, Chile’s smaller population means that, proportionally, its vehicle ownership rate is high. While Argentina has a significantly larger car parc, Chile’s vehicle-to-population ratio is substantial.

Chile’s automotive aftermarket generates over 13 million service visits per year. The car parc is also slightly newer than Argentina’s, with an average age just under 11 years.

Chile presents a business-friendly, highly accessible, and competitive market for those looking to invest or expandin Latin America.

A major challenge for dealerships is to grow in line with an aging vehicle car parc, but there is also a positive outlook—2025 is projected to bring 10% growth in vehicle sales in Chile and 20% in Argentina. This could provide favorable conditions for official networks to find new business opportunities in these South American markets.

BRAZIL

Brazil is massive—not just in size but in its automotive sector. In 2024, Brazil registered 2.4 million passenger vehicles. If you add in light commercial vehicles, that number jumps to almost 3 million, marking an impressive 12.7% growth for two consecutive years. And it doesn’t stop there. As of January 2024, the country had 47.3 million passenger vehicleson the road. And here’s an exclusive for our listeners: as of January 2025, that number has jumped to 48.7 million passenger vehicles, pushing Brazil’s total car parc—including light commercial vehicles—past 55 million cars.

That’s a staggering number, making Brazil a goldmine of opportunities, but also challenges. It’s a country of vast regional differences, domestic production, and unique logistical difficulties. And with rapid market evolution, staying ahead of the trends is key.

One of the defining characteristics of Brazil’s automotive industry? Flex-fuel technology. If you’re not familiar with it, here’s how it works: three-quarters of Brazil’s vehicle car parc can run on 100% ethanol, 100% gasoline, or any mix in between.

And it’s not just about existing cars—84% of newly registered vehicles are flex-fuel. Even gasoline-only cars contain at least 27% ethanol in their fuel mix. This makes Brazil truly unique. Nowhere else in the world has such a high share of ethanol-powered vehicles. This means local manufacturers have had to develop specialized engine parts and even adapt imported cars through a process called tropicalization to handle the ethanol-rich fuel mix.

Another big factor? Sustainability. Unlike gasoline, ethanol is derived from sugarcane, making it a biofuel that is much more environmentally friendly than petroleum-based fuels. This has slowed down the push toward electric vehicles (EVs) in Brazil.

You might hear a lot about electric vehicle growth in Brazil, and yes, the number of registrations is doubling each year. But let’s put that in perspective: in 2024, EVs accounted for just 7.4% of new registrations, meaning only 177,000 of the 2.5 million registered vehicles were electric.

And here’s the kicker: EVs still make up less than 1% of Brazil’s total car parc. So while it’s a hot topic, electrification is still far from becoming mainstream. One major roadblock? Infrastructure. Brazil’s electrical grid and charging network are not yet prepared for a large-scale shift to EVs. Combine that with the government’s ongoing investments in traditional energy sources, and the transition is moving much slower than in places like Europe.

But while EVs are lagging, there’s one area with huge potential: digitalization. Brazil is an interesting case. Consumers here are highly engaged online, with above-average levels of research on auto parts and vehicle maintenance.

The distribution network is still highly fragmented. Repair shops rely on multiple suppliers, each with their own systems, or in many cases, no digital system at all. Instead of ordering online, most mechanics still prefer calling or sending WhatsApp messages to suppliers.

Right now, Mercado Livre is the biggest platform for online auto parts sales, but it’s not optimized for the industry. Unlike in Europe, where you can simply enter a vehicle’s license plate and instantly see compatible parts, Mercado Livre still lacks that level of integration. This leaves huge opportunities for new digital marketplaces to step in and fill the gap.

Beyond digitalization, another area with big potential is repair shop networks and franchises. Unlike the U.S., where large service chains dominate the market, Brazil’s independent repair sector is still highly unstructured. This creates room for buying groups, networks, and new business models to emerge.

And of course, we can’t forget about heavy vehicles and motorcycles. The light vehicle aftermarket might be the biggest, but there’s significant activity in commercial vehicles and two-wheelers as well.

If you’re in the industry, now is the time to pay attention to these trends, whether it’s adapting to Brazil’s aging vehicle car parc, leveraging digital sales channels, or preparing for the slow but inevitable rise of EVs.

This is a market full of potential, but one that requires adaptability and forward-thinking strategies. If you want to stay ahead of the game, follow the trends, invest in digitalization, and keep a close eye on fuel technology shifts. For those interested in more insights, we have a new study launching this year focused on electrified vehicles in Brazil—so stay tuned for that. And don’t forget to check out the GiPA website for more reports and industry analysis.

MEXICO

When we talk about Central America, one thing that stands out immediately is the age of the vehicle car parc. We’re dealing with an aging car parc—significantly older than what we see in developed markets. But here’s where it gets really interesting: the presence of what are known as “rodados” cars. If you’re not familiar with the term, let me break it down for you.

Rodados cars make up about 11% of the total car parc in the region, and they primarily enter through El Salvador before spreading into Guatemala, which, by the way, is one of the most dynamic markets in Central America. Now, here’s the kicker—these vehicles aren’t your typical imports. They’re actually damaged cars from the U.S., mostly from Florida, that make their way through the Gulf of Mexico into El Salvador. Once they arrive, they get repaired and put back on the road—completely legal, fully functional, and an integral part of the regional automotive landscape.

But—and here’s the challenge—rodados cars really shake things up in the aftermarket. Their arrival fragments repair data and complicates the segmentation of the independent sector. Every country in Central America has its own unique market dynamics, and while we try to group them for analysis, the reality is that each has its own set of challenges, characteristics, and opportunities.

Now, shifting gears to another market—Colombia. This country has just under three and a half million vehicles under 3.5 tons, with an average annual usage of around 14,000 kilometers per vehicle. Colombia is a major player in the aftermarket, ranking just behind the big three—Brazil, Mexico, and Argentina—and alongside Peru and Chile in a second tier of key markets.

What makes Colombia stand out is the concentration of vehicles in the northwest, where most of the urban population lives. This geographical factor, combined with the country’s vast distances, creates unique market conditions. And let’s not forget motorcycles! Motorcycles play a massive role in Colombia’s transportation landscape, making them an essential segment of the aftermarket. When it comes to alternative energy vehicles, though, their presence remains marginal at best.

And now, let’s talk about – Mexico. Mexico is in the spotlight for several reasons right now. We’re looking at a circulating vehicle car parc of almost 31 million, with an average annual mileage of 14,000 kilometers. And despite our proximity to the U.S., alternative engines still represent a tiny fraction of the market. Even at double-digit growth rates, our projections show that in 20 years, alternative engines still won’t surpass 10% of the total car parc. That’s something to think about.

More than half of Mexico’s vehicles are over ten years old, which means there’s a massive opportunity for traditional technologies. While new technologies are exciting, let’s be honest—older vehicles still dominate the market, and that’s where a huge portion of the business lies. But here’s another trend we can’t ignore: the growing wave of Chinese vehicles. While we’re still behind Chile in terms of volume, Chinese brands are rapidly gaining traction in Mexico, and they’re already influencing consumer purchasing decisions.

Vehicle registrations surged last year, hitting over 1.5 million—one of the highest in Mexican history. And guess what? A large chunk of that growth comes from Chinese vehicles. Now, does this affect the independent aftermarket yet? Not significantly. But the trend is crystal clear. While alternative engines aren’t taking off as quickly, the increasing number of Chinese brands is something we absolutely need to prepare for. The market is getting more fragmented, with more brands sharing the pie, which means that cataloging and homologation will become more complex.

That’s why we launched ‘The Pulse of the Aftermarket for Chinese Brands’—a new study that’s been a game-changer in understanding how these vehicles are shaping the future of our industry. If you’re in Mexico and working in the aftermarket, this is something you definitely want to check out.

Before we wrap up, I want to touch on something that often confuses people outside of Mexico—the term “chocolate cars.” If you’ve ever come across this term and thought it was a typo, let me assure you, it’s not. In Mexico, “chocolate cars” refer to vehicles that enter the country from the U.S., either legally or illegally. These second-hand cars are sold at rock-bottom prices in the U.S. and then resold in Mexico at a profit. They account for about 20-25% of the total car parc and play a massive role in the aftermarket—sometimes through organized networks, sometimes through individual resellers. If you’re operating in northern Mexico, near the U.S. border, you’re definitely familiar with this phenomenon.

Challenges & Opportunities for Industry Players

- Adapting to the aging vehicle car parc: Expansion of parts and service networks will be necessary to meet demand.

- Chinese brand expansion: Opportunities exist in OEM and IAM markets to support a growing multi-brand ecosystem.

- Digitalization: Strengthening online parts distribution and e-commerce models to enhance accessibility and efficiency.

- Electrification & Infrastructure: While slow, the transition is inevitable; stakeholders must prepare for long-term investments in service capabilities and charging networks.

Conclusion

Latin America’s automotive aftermarket is poised for significant growth but remains highly diverse across different markets. Companies that adapt to car parc aging, digital transformation, and evolving brand preferences will find opportunities for sustainable growth. The webinar underscored the importance of localized strategies, investment in digital tools, and supply chain adaptation to navigate the complex yet promising landscape of Latin America’s aftermarket industry.